A Look Into Today’s IPO Environment

Innovation, IPOs, and Private Markets: Considering the Intersection

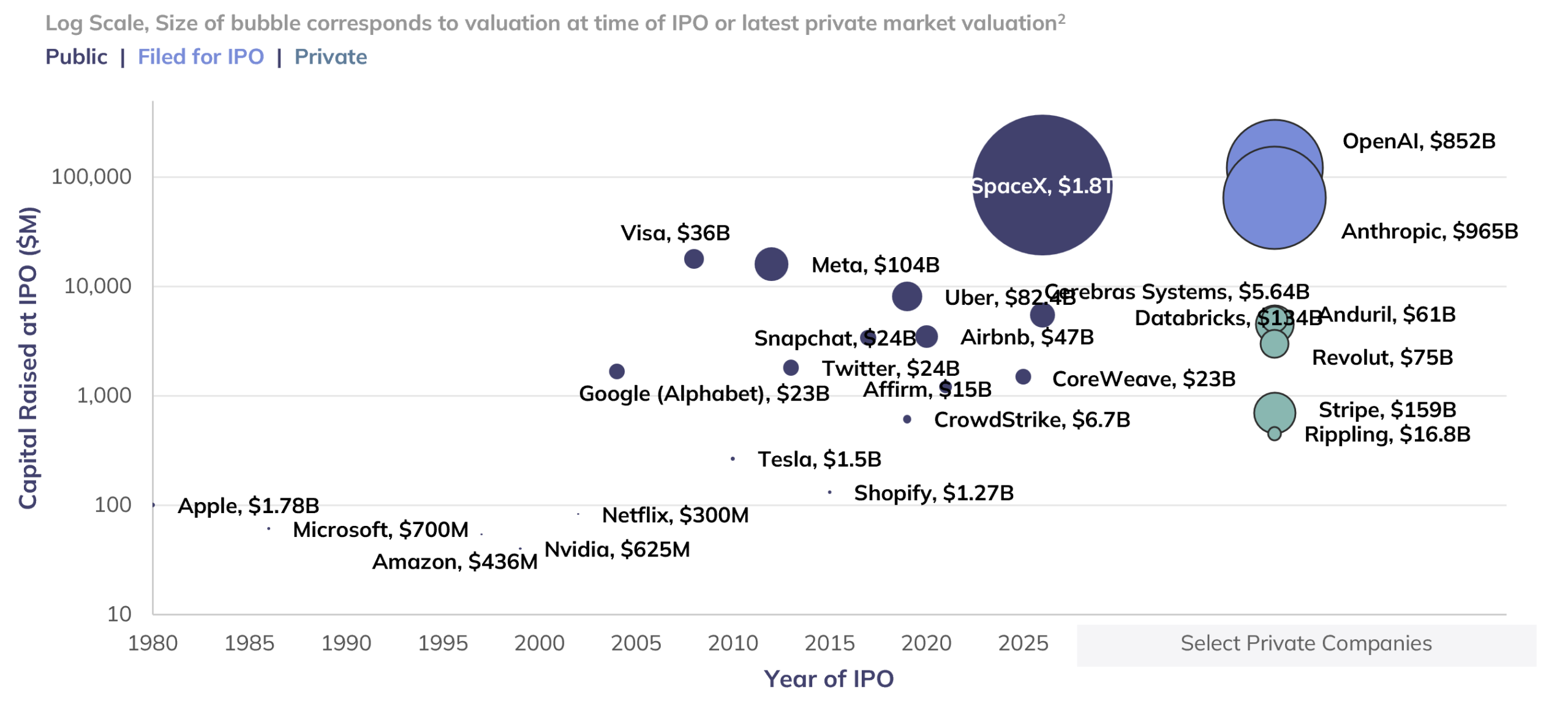

After several years on the sidelines, the IPO market has reawakened in 2026. Analysts project that US IPO proceeds could reach a record $160 billion this year, in large part driven by SpaceX’s recent June debut. The company’s listing was a landmark event, raising more than $85 billion – crowning the largest IPO in history, more than triple the previous record set by Saudi Aramco in 2019.1

SpaceX is part of a broader resurgence in high-profile IPOs. Cerebras Systems and CoreWeave have already drawn attention to strong demand for AI-related listings, compounded by anticipation of future offerings from companies such as OpenAI and Anthropic. This reflects a deep pipeline of companies tied to some of the defining growth themes expected over the next decade – businesses sitting at the intersection of artificial intelligence, data infrastructure, aerospace, and next-generation industrial innovation.

The renewed IPO energy has drawn significant excitement from investors seeking access to transformational businesses. From an investment perspective, however, the most important question is not whether these companies are compelling, but whether the IPO is the most attractive point of entry. For investors today, companies are increasingly growing at extraordinary rates in the private markets long before their public listing.

Over the past few decades, we have observed companies raising more capital privately, remaining private longer, and reaching far greater scale before entering public markets. As a result, the IPO has evolved. In many cases, it is no longer the beginning of a company’s growth journey, but a later-stage liquidity event – one that provides broader availability only after a significant amount of value creation has already occurred.

Historically, public markets played a central role in funding corporate growth and technological development. The IPO was often the point at which young, fast-growing companies – the likes of Apple, Amazon, and Google – raised capital to expand their businesses, build infrastructure, and pursue new markets. Public shareholders were helping fund the next stage of development, and IPOs often gave investors early access to growth.

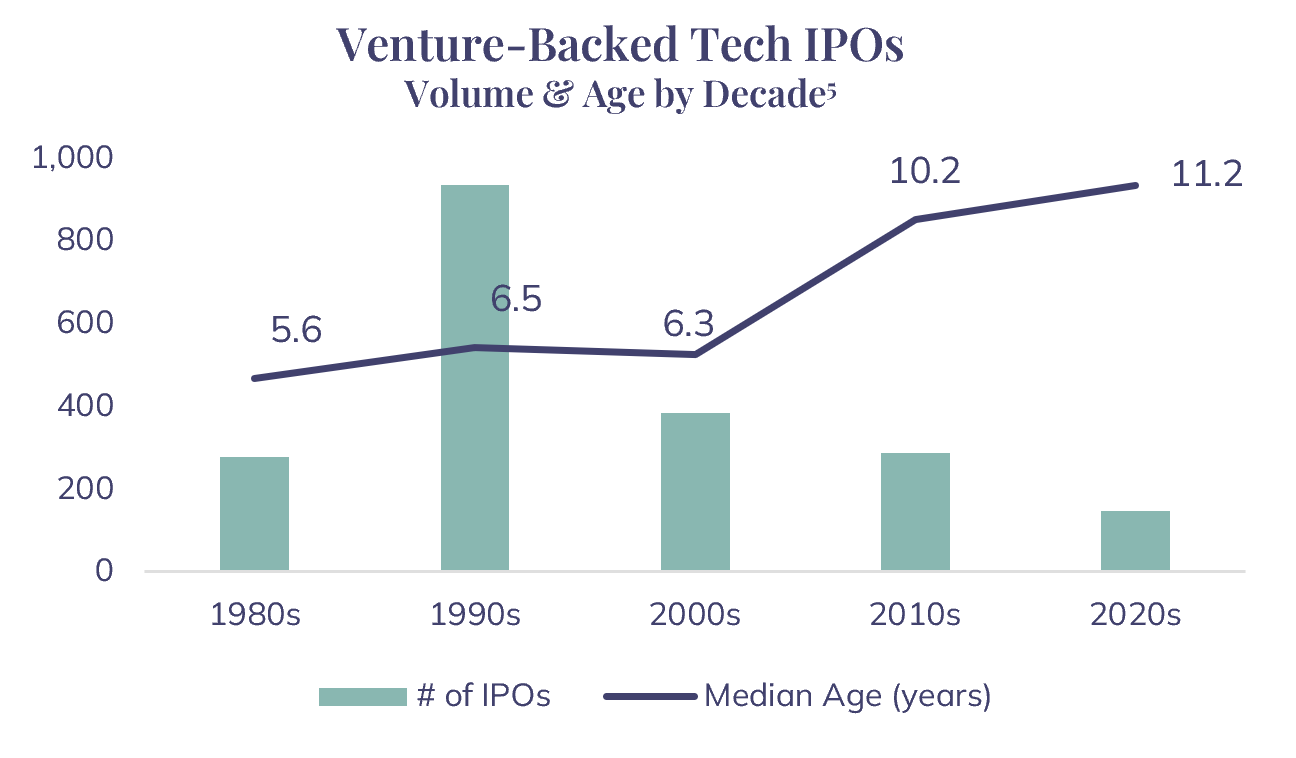

Today, companies often remain private through their most rapid stages of scaling. The modern IPO frequently occurs after a company has already raised multiple private financing rounds, reached global scale, and attracted a broad set of institutional investors. In that sense, the IPO has become less of a growth-funding necessity and more of a liquidity and market-access event. Venture-backed businesses, on average, take over 11 years before they IPO.

While public markets still provide important exposure to established leaders, they no longer represent the full opportunity set for innovation. A growing portion of the most dynamic value creation is taking place before companies become public, which often means the most powerful investment opportunity may be while the company is still developing and scaling outside the public spotlight. Increasingly, accessing innovation through private market investments is critical to capture the greatest growth potential.

Private Companies Increasingly Going Public at Outsized Valuations

Log Scale, Size of bubble corresponds to valuation at time of IPO or latest private market valuation2

Then Versus Now: Public Investors Access More Mature Companies

The path from innovation to scale has changed meaningfully over the past two decades. Take Amazon, Google, and Facebook. Today, these companies represent more than $8 trillion in combined market value and stand as pillars of the “Magnificent 7.” But at the time of their IPOs, they were still early in their journey as high-growth businesses with much to prove, still refining their models, and working toward durable monetization. Amazon, for example, went public back in 1997 as an e-commerce bookstore, long before its transformation into one of the world’s largest companies – spanning retail, logistics, and cloud computing – all while in the public markets.

Below, we highlight this development by reflecting on some of today’s largest, most well-established companies at the time they first entered the public markets. Times have changed from the speculative, internet-enabled businesses to the Uber and Airbnb era – where companies had been staying private longer and listing as scaled global platforms. This trend that has been amplified further in today’s market, where the modern IPO often comes after significant capital formation and value creation.

Many of today’s highest-profile private companies are approaching public markets at valuations that would have been nearly unimaginable in earlier IPO cycles. SpaceX just went public at a $1.8 trillion valuation – launching it to the sixth largest US public company by market cap. OpenAI and Anthropic have both raised hundreds of billions of dollars of private capital at valuations closing in on $1 trillion as well – reflecting a deeper change in where companies are in their lifecycle when public investors first gain access.

Evolution of Notable IPOs and Their Public Market Transformation3

Late 1990’s & Early 2000’s to Today’s Modern IPO

| Amazon | •1997 IPO: Raised ~$54 million at a $438 million valuation. The company was more simply an early-stage internet bookseller. •Today: One of the world’s largest companies – spanning retail, logistics, cloud computing, advertising, media, and artificial intelligence infrastructure. |

| Netflix | •2002 IPO: Raised ~$83 million at a ~$300 million valuation. At that point, the company was still an early-stage online DVD rental business. •Today: One of the world’s largest entertainment platforms – spanning streaming, original content, global distribution, advertising, gaming, and live programming. |

| •2004 IPO: Valued at ~$23 billion, a substantial valuation at the time but still only a fraction of the size of global leaders like General Electric and ExxonMobil (both ~$300B market caps). •Today: One of the world’s largest companies. Expanded from search into digital advertising, mobile operating systems, cloud infrastructure, video, maps, and artificial intelligence. | |

| •2012 IPO: Went public later in its lifecycle than Amazon or Google, at a valuation of ~$104 billion. Even then, important elements of its business model were still maturing. •Today: Its advertising platform, mobile monetization, and broader technology platform have evolved meaningfully after the IPO. | |

| Uber | •2019 IPO: A globally scaled platform at the time of its IPO, valued at approximately ~$82 billion. Uber had already built significant brand recognition and expanded internationally. •Today: A mature global mobility and delivery platform. While the business has continued to evolve as a public company, much of the early platform creation occurred while Uber was still private. |

| Airbnb | •2020 IPO: The mature global travel marketplace went public at a ~$47 billion valuation, spanning short-term stays, longer-term stays, experiences, and a large host network. •Today: Like Uber, Airbnb entered the public markets after already achieving meaningful global scale in the private markets. |

| SpaceX | •2026 IPO: Scaled aerospace, satellite communications, and infrastructure platform. The company’s valuation rivals the largest businesses in the world. |

The Value of Being Early: Why Companies Stay Private Longer

So why are companies staying private for longer? Several structural forces have contributed to this shift where many companies no longer need public markets as early in their development as they once did.

Operating Flexibility

Remaining private allows companies greater flexibility to pursue long-term innovation without the disclosure requirements and quarterly scrutiny that comes with being a public company.

SpaceX illustrates the point well: its progress required years of experimentation, engineering iteration, and capital-intensive testing to overcome failure. That type of development path can be difficult to manage under the constant visibility and short-term scrutiny of public markets.

Capital-Intensive Innovation

Today’s innovation cycle extends beyond just AI into capital-intensive areas such as data infrastructure, advanced manufacturing, aerospace & defense, life sciences, and energy systems.

Unlike the software-led cycle of the 2010s, many opportunities today are tied to physical infrastructure and longer development timelines – requiring patient private capital for companies whose long-term potential may not yet be reflected in near-term financial results.

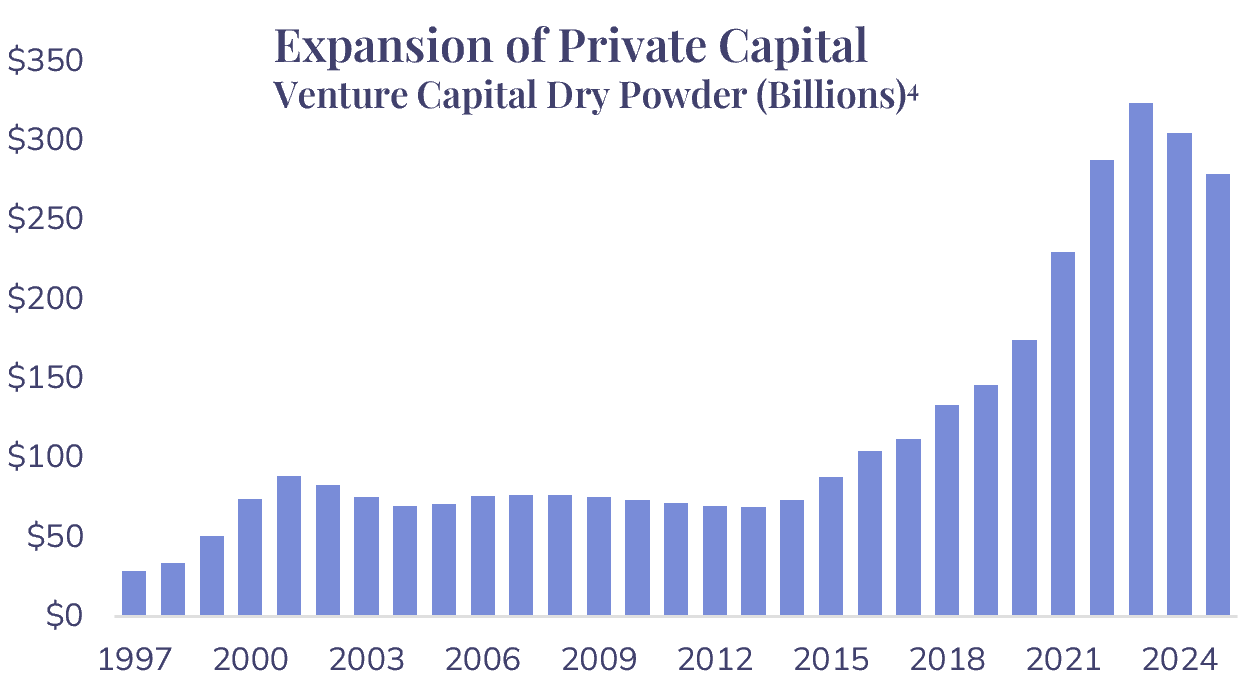

Availability of Private Capital & Increased Private Market Liquidity Channels

The private capital ecosystem has matured, and companies today have access to a much deeper and more diverse pool of funding than they did in prior decades. Venture capital, growth equity, private equity, sovereign wealth funds, hedge funds, family offices, and other institutional investors now provide capital across a company’s lifecycle.

With deeper pools of capital available companies can now raise significant funding privately – allowing them to continue investing in product development, infrastructure, hiring, acquisitions, and market expansion without pursuing an IPO.

The growth of secondary transactions, tender offers, and private share marketplaces has also reduced the need for an IPO as the primary source of liquidity.

Stripe is a good example of this evolution – having used tender offers and secondary transactions to provide liquidity to employees and shareholders without needing to rely on a public listing as the only exit path.

Together, these forces have created a new equilibrium. Companies can raise more capital from private investors, access more flexible funding, provide interim liquidity to stakeholders, and remain focused on long-term development for longer periods of time. As a result, many companies are reaching much greater scale before they become public. For investors, the implication is significant: a growing share of value creation is occurring before companies enter public markets. The IPO may still be an important milestone, but, in many cases, it now represents broader access to a company that has already scaled substantially.

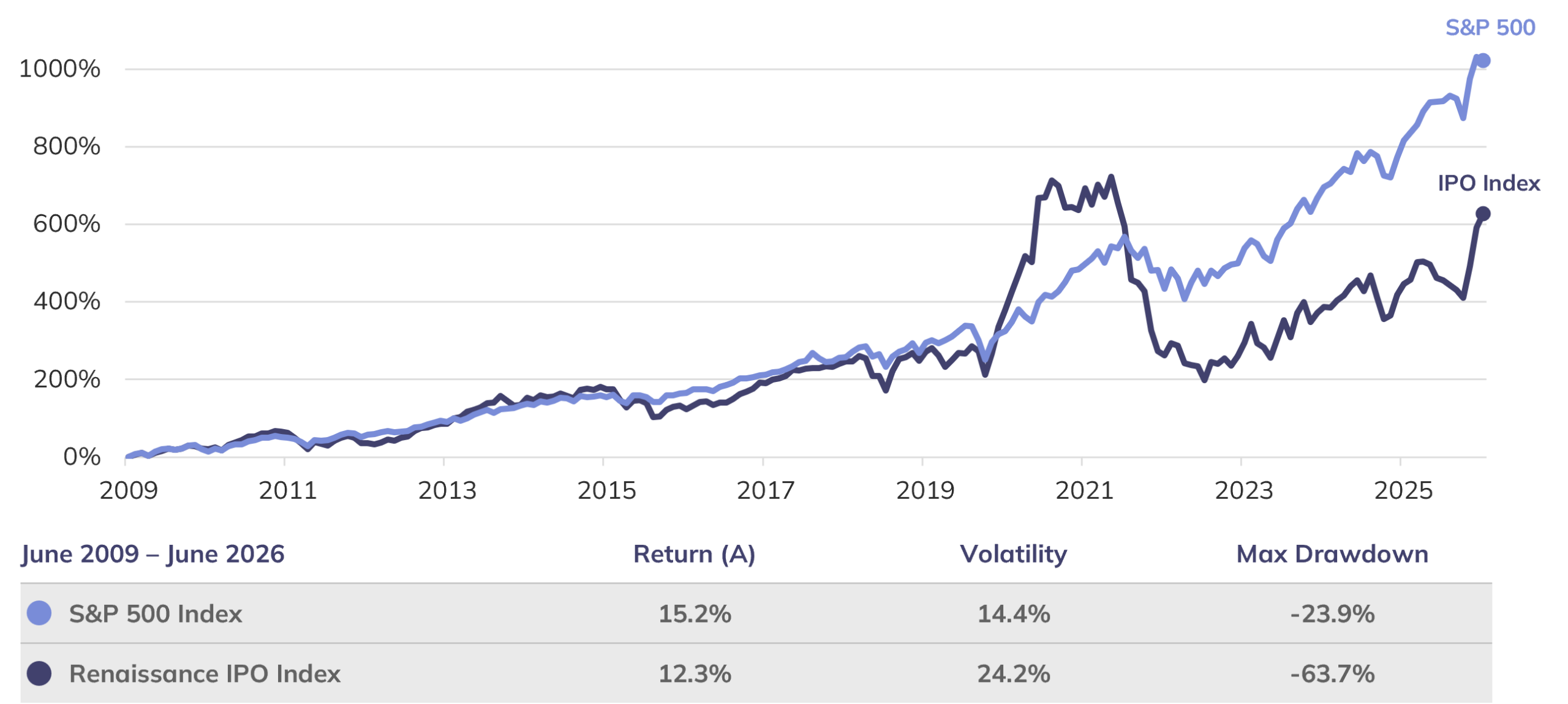

IPO Outcomes: Headlines Often Overstate the Opportunity

The visibility of IPOs can make them feel like “can’t miss” opportunities, but history suggests that IPO investing requires caution – and a willingness to stomach risk. While first-day IPO “pops” often receive the most attention, on average the long-term performance has generally been less compelling.

Index data shows that IPOs have underperformed the market by about -3% annually since June 2009 (12.3% for the Renaissance IPO Index vs. 15.2% for the S&P 500), while also exhibiting much higher volatility and much steeper drawdowns. Further, when controlling for differences in size and valuation, US IPOs have trailed comparable public companies with similar market caps and valuations over the next one, three, and five years after listing, on average.

Investors who do opt to participate in recently transitioned public companies should be prepared to withstand a bumpy ride. There are countless examples of notable, sought-after IPOs that experienced substantial drawdowns – declines of -55% or greater are common in just their first year of trading – even when the underlying businesses were well known and viewed as strategically important.

This should not be surprising as IPOs often occur when market conditions are favorable, investor demand is strong, and private holders are seeking liquidity. That combination can create a challenging setup for new public market buyers – which can be further exacerbated as post-IPO lockups expire and early investors seek to offload their shares, creating additional selling pressure several month after listing.

The takeaway is not that investors should avoid all IPOs. Rather, it is that IPOs must be evaluated with the same discipline as any other investment. A great company can still be a challenging investment if the entry point and valuation already reflects outsized expectations.

IPO Performance is Highly Volatile

Select Company Max Drawdown First year Post-IPO6

| Company | Year of IPO | Year 1 Max Drawdown |

|---|---|---|

| Amazon | 1997 | -30% |

| Nvidia | 1999 | -36% |

| Netflix | 2002 | -71% |

| 2004 | -17% | |

| Visa | 2008 | -52% |

| Tesla | 2010 | -39% |

| 2012 | -54% | |

| 2013 | -58% | |

| Alibaba | 2014 | -49% |

| Shopify | 2015 | -52% |

| Snap | 2017 | -56% |

| Uber | 2019 | -68% |

| CrowdStrike | 2019 | -67% |

| Snowflake | 2020 | -52% |

| Palantir | 2020 | -53% |

| Airbnb | 2020 | -39% |

| Affirm | 2021 | -65% |

| Coupang | 2021 | -64% |

| Rivian | 2021 | -88% |

| Arm Holdings | 2023 | -43% |

| CoreWeave | 2025 | -65% |

| Circle | 2025 | -81% |

| Cerebras | 2026 | -40% |

| Median | -53% |

IPO Basket Has Lagged the Broad Market While Taking More Risk7

As of 6/30/2026

Endnotes

1 Goldman Sachs base-case forecast for 2026 U.S. IPO proceeds, as reported by Reuters, February 9, 2026.

2 Source: Company press releases, SEC filings, Reuters, CNBC, Forbes, Axios, TechCrunch, Pitchbook, and other public market reporting. IPO valuations generally reflect reported market capitalization or fully diluted valuation at IPO pricing; figures are rounded.

3 Details on notable IPOs sourced from company’s Investor Relations websites, CNN, Forbes, CNBC, Reuters, and BBC; figures are rounded.

4, Sourced from Pitchbook NVCA Venture Monitor.

5 Source: VanEck. Jay R. Ritter, Director – The IPO Initiative; University of Florida. March 17, 2026.

6 Sourced from Bloomberg and Morningstar.com

7 Data sourced from Bloomberg. Returns are annualized from January 2009 – June 2026.